If you want one simple number to show how well your procurement team is performing or where money is being lost, that number is purchase price variance. It is a key measure in procurement tracking, and every supply chain manager should understand it thoroughly.

In the modern manufacturing setting, purchase price variance in procurement serves as the principal litmus test of the efficiency of your purchasing process. This metric connects the purchasing department with the financial goals. By keeping tabs on it, you are not just observing expenditures, but you can also monitor your procurement tracking system.

In this guide, Pro Procurement explains everything about purchase price variance, sources of variance, and ways of reducing it. If you handle a logistics operation or commodity sourcing, this article is for you.

The Core Concept: What Is Purchase Price Variance (PPV)?

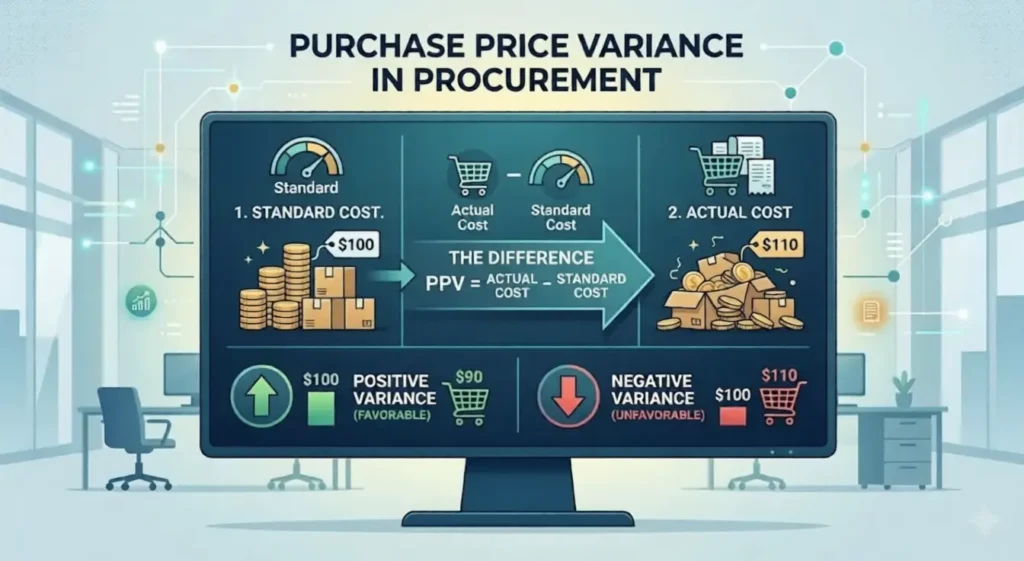

The difference between the planned cost and the actual cost is known as purchase price variance (PPV). Moreover, it is the financial difference between the actual price paid to the suppliers for commodities or services and their standard costs. It needs to be controlled to ensure profit margins.

Key terminology you need to know:

● Standard Cost

Standard cost (Budgeted Price) refers to the predetermined price at which a company plans to acquire its products. This price is determined in the budgeting process through past prices, market conditions, and agreements with suppliers.

● Actual Cost

Actual cost (Actual Price) is the real price paid when the company buys the product. This price can change because of market conditions, supplier changes, order size, or urgent purchases.

● Market Fluctuations

Market fluctuations are changes in prices caused by outside factors like changes in commodity prices, currency rates, global events, or supply and demand. These changes often lead to differences between planned and actual costs.

The Role of Standard Cost

The standard cost refers to an estimated amount determined at the start of the accounting period. It is not just any figure; rather, it is a well-planned amount that can help in future cost estimates. The difference between the actual cost and the standard cost results in a variance. The variance indicates the management’s effectiveness in dealing with market conditions and the stability of suppliers’ prices amid rising global prices.

PPV and the P&L Statement

The P&L statement reveals changes in the Cost of Goods Sold (COGS). If prices go up, the COGS will also go up, and the gross profit will be negatively affected. If it is positive, it reduces the cost of goods sold and increases net income.

Raw materials constitute a significant portion of production costs. A minor fluctuation in the per-unit cost of raw material can have a substantial financial effect on its production value. Finance departments monitor PPV closely at each period due to its effect on profitability.

The PPV Formula Explained in Simple Terms

To control what you measure, you must quantify the impact of price changes. The PPV formula is the standard equation used by procurement teams to quantify price performance. It is a widely used method to quantify the effects of price changes in dollars. It is one of the most important equations in procurement accounting:

The Standard Calculation

The basic formula for realized variance is:

PPV = (Actual Price – Standard Price) × Actual Quantity

The Forecasting Component

Forecasted PPV = (Forecasted Price – Standard Price) × Forecasted Quantity

Worked Example: 5,000 Units of Raw Material

| Metric | Value | Notes |

| Standard Price (SP) | $10.00 per unit | Budgeted rate set at the start of the year |

| Actual Price (AP) | $11.50 per unit | Invoice price after market increase |

| Actual Quantity (AQ) | 5,000 units | Purchase order volume |

| Price Difference | $1.50 per unit | AP − SP = $11.50 − $10.00 |

| Total PPV | $7,500 Unfavorable | $1.50 × 5,000 units |

Here, the organization has exceeded its budgetary expenditure by $7,500. This is a “positive” numerical answer but an “unfavorable” business situation.

Favorable vs. Unfavorable Purchase Price Variance

In the world of purchase price variance, the sign of the result determines the narrative.

Favorable Variance (Negative PPV)

A negative result occurs when the actual price is lower than the standard price. This is generally considered a “savings.” It reduces the cost of goods sold and expands the gross margin.

Unfavorable Variance (Positive PPV)

A positive result means you paid more than budgeted. This “unfavorable” outcome hits the bottom line directly, eroding the profitability of the products being manufactured.

The “Cheap Isn’t Always Better” Nuance

While a negative PPV is often used as a performance measure for buyers, it can be a simplistic view. A favorable variance might look good on a spreadsheet, but if it was achieved by buying sub-par materials, the company may face:

- Production Delays: Lower-quality materials often break during manufacturing.

- Higher Scrap Rates: Cheap parts lead to more rejected finished goods.

- Warranty Claims: If the final product fails for the customer, the “savings” are quickly erased by repair costs.

Let us take the case of a business purchasing steel for $0.80 per kg less than the estimated price. This leads to a favorable PPV of $40,000. However, after acquiring the product, it fails to meet its quality requirements during the manufacturing process. Consequently, it results in rework, delay, and ordering at a high price. The $40,000 in ‘savings’ was quickly eclipsed by $135,000 in rework and delays, resulting in a net loss of $95,000. This illustrates the importance of considering other factors alongside PPV.

Why Tracking Purchase Price Variance Matters in Procurement

Purchase price variance (PPV) in procurement is not just a number in reports. It helps guide important business decisions.

Budget Integrity

Integrity of the budget refers to the process of maintaining accuracy within the budget. The tracking of PPV allows the finance team to adjust the estimate on a timely basis. Without tracking, even minor changes in costs may lead to major issues, affect planning and strategy.

Supplier Performance Management

Supplier performance management uses PPV to evaluate which suppliers adhere to the price agreement. It helps identify the suppliers who maintain their prices based on the contractual agreement and those who gradually raise their prices. When a particular supplier continuously shows an unfavorable PPV, then it is time for a contract review or a supplier change.

Inventory Valuation

Valuation of inventories is associated with the recording process in the accounting system. In the standard cost accounting system, inventory is valued according to the standard cost, not the actual cost. The PPV account records the difference between these two, which helps keep financial statements correct. This is why auditors and CFOs pay close attention to it.

Procurement Team Accountability

Accountability of the procurement team measures how well the procurement team performs. With PPV, the management can make a fair assessment of their performance. Procurement teams that maintain PPV within favorable limits demonstrate effective cost management and strategic sourcing practices.

The Root Causes: Why Does Variance Happen?

To understand PPV, you need to look at the main reasons why prices change. These reasons usually fall into two groups: market factors and internal issues.

External Market Factors

External market factors are things that companies cannot control. These include the fluctuating prices of raw materials such as steel, oil, or semiconductors because of supply and demand in the international marketplace. Another external market force is inflation, which raises the price of all goods. Other factors can be new taxes, trade barriers, etc.

- Inflation in commodity prices (oil, steel, semiconductors)

- Changes in currency exchange rates leading to higher import costs

- Unexpected increase in tariffs and other import costs

- Political instability leading to supply shortages

- Lack of raw materials is forcing spot prices

- Increased freight/logistics expenses (ports, fuel)

Internal Operational Inefficiencies

Internal operational inefficiencies are problems within the company. Mismanagement in planning causes poor forecasting and results in the purchase of materials at a higher price. Similarly, rush deliveries result in high expenses because rapid transportation services such as air freight are relatively more expensive than normal delivery processes. Maverick spending is another problem faced by firms, whereby certain teams purchase supplies from other suppliers at higher rates than the standard rate.

- Inaccurate forecasting is causing last-minute procurement.

- Rushed orders with high shipping rates

- Maverick Spending: purchases made outside of negotiated contracts

- Inadequate standardization of costs

- Lack of vendor consolidation is reducing bargaining power

- Poor contract management resulting in negative rates

Using a PPV Calculator As A Professional Tool

Modern procurement teams use ERP systems like SAP or Oracle to track Purchase Price Variance (PPV) automatically. These systems compare the purchase order with the invoice and check the prices. If there is a difference, it is highlighted, making it easy to see cost changes and control spending. It allows the procurement department to take immediate action in adjusting its selling prices.

How to Build a PPV Calculator in Excel

You can make a simple PPV calculator in Excel to check cost differences easily. First, add columns for Standard Price, Actual Price, and Quantity. Then enter the purchase values in each row.

Next, find the price difference by subtracting the Standard Price from the Actual Price. After that, multiply the price difference by Quantity to get PPV. In the end, you can mark the result as “Favorable” if it is negative or “Unfavorable” if it is positive.

How PPV is Recorded

Accountants treat purchase price variance as a vital indicator of budget integrity. They record it in the General Ledger (GL) to keep financial records accurate. This helps show inventory at its “Standard” cost, while also tracking the real “Actual” money spent.

Most organizations use this unique GL code to identify the price variance, so that the finance department can monitor it individually. Every month, the PPV balance is analyzed and evaluated, and it helps in budget planning for future operations.

Debit and Credit Flow

- Unfavorable Variance: This is recorded as a Debit. It acts as an expense that increases the cost of sales.

- Favorable Variance: This is recorded as a Credit. It acts as a reduction in expense, effectively boosting net income.

Standard cost is used for accounting for the raw materials inventory account. In this case, the values of the inventories remained constant regardless of any changes in the market. The PPV account is used to record the difference between the standard and actual cost and will appear under Cost of Goods Sold in the income statement. Unfavorable PPV is recorded as a debit to the variance account, increasing the Cost of Goods Sold (COGS).

Scenario: You purchase 5,000 units of raw material at an actual price of $11.50 per unit, against a standard cost of $10.00 per unit.

Through recording such variations in a specific account, the financial team prepares reports referred to as the margin bridge. This report explains the reasons behind the change in profit margins, isolating the effects of price performance from volume fluctuations.

| Account | Debit (DR) | Credit (CR) |

| Raw Materials Inventory (5,000 × $10.00) | $50,000 | – |

| Purchase Price Variance (Unfavorable) | $7,500 | – |

| Accounts Payable (5,000 × $11.50) | – | $57,500 |

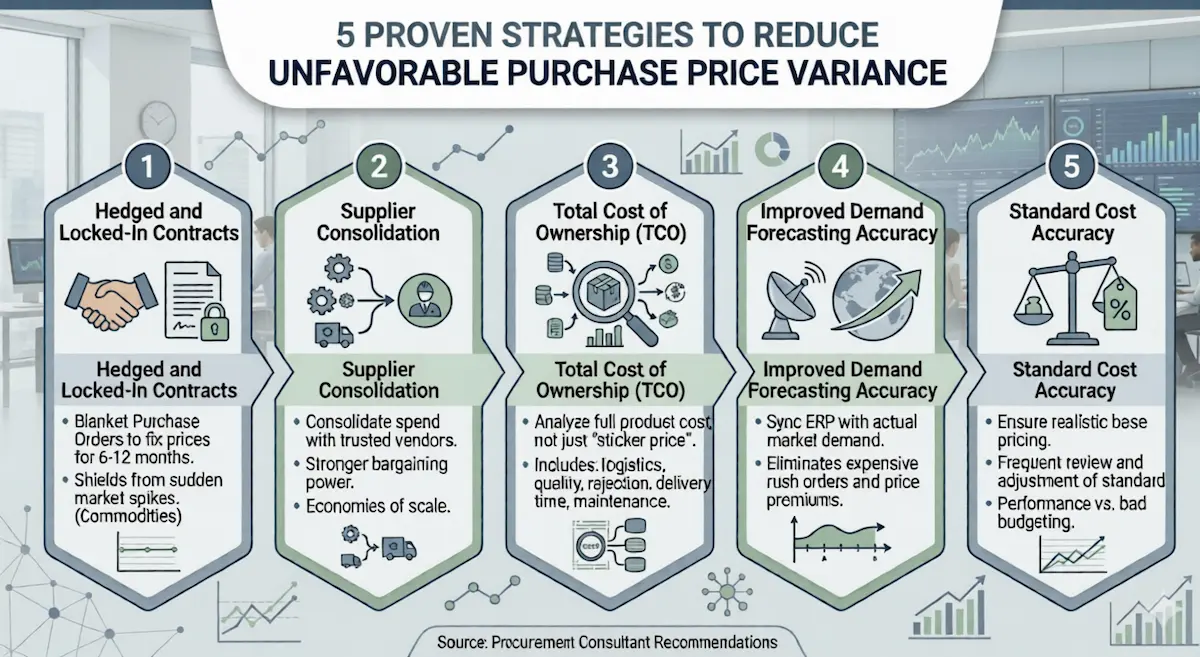

5 Proven Strategies to Reduce Unfavorable Purchase Price Variance

To move from tracking variance to controlling it, procurement consultants recommend several actionable strategies:

1. Hedged and Locked-In Contracts

Use “Blanket Purchase Orders” to lock in prices for 6-12 months. This shields the budget from sudden market spikes. This is especially effective for commodities with high price volatility, such as copper, plastics, and energy.

2. Supplier Consolidation

By reallocating your spending towards trusted vendors, you increase your bargaining power through economies of scale. Higher volumes equal stronger price commitments. This is one of the fastest ways to move unfavorable PPV in the right direction.

3. Total Cost of Ownership (TCO) Analysis

It means looking at the full cost of a product, not just the buying price. Don’t only focus on the “sticker price.” A slightly higher price can still be better if it reduces other costs. These include delivery (logistics), product quality issues or rejection, delivery time, payment terms, and long-term maintenance costs. TCO helps you choose the option that is cheaper and better over the full life of the purchase.

4. Improved Demand Forecasting Accuracy

Rush orders are one of the most controllable sources of unfavorable PPV. By syncing your ERP with actual market demand, you eliminate the need for expensive “rush orders” that carry a price premium.

5. Standard Cost Accuracy

Unfavorable variances occur when the standard pricing is too low to begin with. Frequent review and adjustment of standard costs make sure that variances reflect performance rather than bad budgeting practices.

Stop losing money to market spikes. Visit proprocurement to implement TCO analysis, lock in contracts, and master PPV control. Optimize your procurement strategy today and shield your budget from unfavorable variance

PPV vs. Other Procurement Metrics – Know the Difference

Many procurement teams often mix up these three metrics, but they are actually different. Each one measures something specific. The table below explains each metric in a simple way, so it is easier to understand the difference.

| Metric | Focus | P & L Impact | Strategic Value |

| PPV | Actual vs. Budgeted Price | Direct (hits Cost of Goods Sold) | Measures budget integrity and price performance. |

| Cost Avoidance | Price Paid vs. Market Increase | None directly (prevents future loss) | Measures the “damage” prevented by procurement. |

| Spend Under Management | % of Spend controlled by Procurement | Indirect (enables better PPV control) | Measures the maturity of the procurement function. |

The Bottom Line

Purchase price variance is not just a number in a spreadsheet. It plays an important role in long-term profit. In manufacturing, materials make up a large part of total costs, so understanding the PPV formula is very important. Through investigating the reasons for price variations resulting from market dynamics and internal factors, companies can take action to control costs and protect their profit margins.

By reducing the unfavorable PPV, the purchasing department is not only cutting costs but also ensuring that the firm remains financially strong. This assists in enhancing supplier relationships and providing the management team with a better understanding of the company’s operations. That is the true value of getting purchase price variance right.

Ready to Get Your PPV Under Control?

Pro Procurement helps supply chain teams manage costs in a smarter way. It supports everything from setting standard costs to improving supplier negotiations. If you want to improve cost control and performance, let’s discuss how we can help.

Contact Pro Procurement at info@proprocurement.us or call +1 347-480-1111.

Frequently Asked Questions

What does PPV stand for?

PPV stands for Purchase Price Variance. It shows the difference between the planned price and the actual price paid for goods. It is used in procurement and accounting and is included in Cost of Goods Sold to track cost changes.

Is a negative PPV good or bad?

A negative PPV is an indication of good performance as the cost is lower than expected, thus improving profits. However, sometimes low cost can result in low-quality products and poor supplier performance. So it must be checked with quality and supplier performance.

How often should standard costs be updated?

Standard costs are usually updated once a year. Some firms revise their standards on a quarterly basis, while others may even revise them on a monthly basis for certain materials. This helps keep budgets accurate and improves financial planning.

How does technology improve PPV tracking?

Current ERP solutions automatically generate PPV through the linkage between purchase orders and invoices. This not only minimizes potential errors but also ensures up-to-date cost information. This makes it easy for procurement departments to respond quickly to changes in prices.

What is the relationship between PPV and budgeting accuracy?

PPV helps measure how close actual purchase costs are to the budget. A high PPV indicates ineffective budgeting or alteration of prices. If it is low, it means forecasts are accurate, and spending is well controlled across procurement activities.